![[keyword]](https://learnxyz.in/wp-content/uploads/2026/02/Would-you-put-your-money-in-a-100-year-bond.jpg)

Google’s parent, Alphabet, just issued a 100-year bond. So in today’s Finshots, we tell you why anyone would buy something they’ll never live to see paid for in full.

But before we start, if you are someone who likes to keep track of what is happening in the world of business and finance, then press subscribe if you haven’t already. If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

In 1997, Motorola issued a 100-year bond. In simple terms, it borrowed money from investors and promised to repay the principal only after a full century. It was widely seen as the last century bond by a technology firm, although, technically, Rockwell Automationa software company, issued one a year later. Still, we’ll stick with Motorola, since it’s the name most of us recognize.

Motorola raised $300 million at an interest rate of 5.22%. This meant that even if it paid back the borrowed amount only after 100 years, it had to pay bondholders 5.22% interest every year, regardless of how interest rates moved over time.

And at the time it was not unusual. In fact, in 1997, a record 41 century bonds were issued as yields (interest rates) on long-term 30-year US Treasuries fell sharply (from 7.8% in 1994 to around 5% by the end of 1997). And as rates fell, tech companies riding the dot com boom snapped up long-term debt at relatively cheap rates before conditions changed.

In hindsight, it wasn’t a bad call. Recent long-term Motorola bonds are now trading at yields closer to 6%. Yet the company is still only paying 5.22% on that 1997 bond. This is because bond prices and yields move in opposite directions – when yields rise, bond prices fall, and vice versa.

Sidebar: The simple logic behind this is that if interest rates rise and new bonds start offering higher coupon rates (the interest paid on the bond’s face value), the bond you hold suddenly looks less attractive. So if you want to sell it before it expires, you’ll probably have to offer it below face value to tempt buyers.

On the other hand, if interest rates fail, your mortgage becomes more attractive. Buyers may then be willing to pay more than its face value to own it.

The only reason it has been labeled so problematic by investors like Michael Burry is that when Motorola issued that 100-year bond, it was a top-25 company in America by market cap and revenue. At one point it was ranked number 1 in the US, even before Microsoft. But fast forward to today, it’s in 232nd place, with only about $11 billion in sales. It has lost dominance in the very business that made it famous – mobile phones, but it still has to pay off that debt until 2097.

This is exactly why 100-year bonds are not a popular way to raise money right now. As a company, you don’t know if you’ll even be around a century from now. And even if you do, whether your business still matters. Take the example of JC Penney, an American retail chain. It issued a $500 million bond in 1997 and went bankrupt just 23 years later. Sure, bondholders do get paid before shareholders in the event of a shutdown, but it’s still a serious risk.

And yet you’ve probably seen the news. Alphabet, Google’s parent company, recently £1 billion borrowed by issuing a 100-year bond in the European market. And the demand was almost 10 times more than what Alphabet offered.

It’s not the only bond Alphabet has sold. It also issued shorter-term bonds maturing between 3 and 32 years, mostly in pounds and Swiss francs. But interestingly, it is the 100-year bond that has attracted the most interest from investors.

Which of course raises two questions. Why is Google issuing something as rare as a 100-year bond, and that too in the European market? And who on earth buys it?

After all, as an investor, you are not going to be there when this bond finally matures. So what exactly are buyers planning to do with something they’ll never pay back in full?

Let’s answer the first question first.

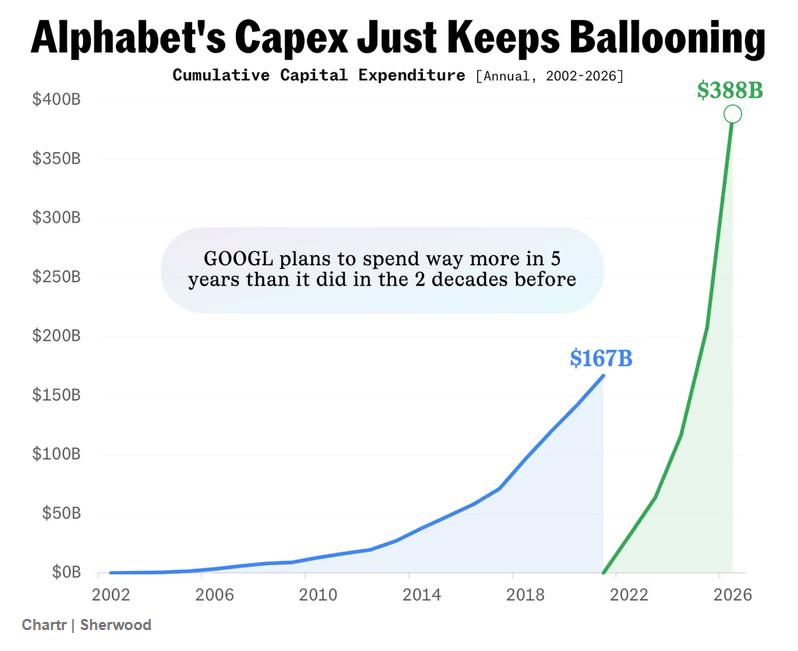

Alphabet plans to spend $185 billion in capital spending this year, largely on AI infrastructure, data centers and next-generation technology. Now sure, it generates more than $73 billion in free cash flow annually and has about $126 billion in cash on its books. But it cannot simply drain its reserves. These investments will span years, and he knows more funding will be needed along the way. In fact, its planned capital investment for 2026 alone will push up its total spending over the past five years to almost double what it spent in the two decades to 2018.

But the reason it’s chasing a 100-year bond is probably because for one in a 6.125% interest rate for a very long time, regardless of where rates go in the future. Another reason is demand. British pension funds and insurance companies are actively looking for long-term bonds. They have obligations such as pensions, insurance payouts, endowments, that stretch decades into the future. And long-term bonds fit that need perfectly, because they give them a steady income for many years. This is also why other US companies such as Thermo Fisher and Caterpillar have recently issued long-term bonds in Swiss francs. Europe has large investors who prefer lending in their own currency.

For Alphabet, there is also money spreading its loans across different markets. If currency movements work in its favor, its effective cost of borrowing in dollars may even fall. Of course, currencies can also move the other way around. But there are ways to hedge that risk—just not something we’ll get into in this story.

Well, that answers both questions. Large institutions with long-term liabilities like to buy these bonds because they match their future payouts. But that doesn’t mean regular investors can’t buy them too. Which raises another interesting question. What exactly do they do with something that lasts 100 years?

See, investors don’t always buy a bond just to hold it to maturity. There are other reasons too.

One is generational wealth. You buy a 100-year mortgage and earn interest every year. When you are gone, your family continues to receive that income. And whoever is in the 100th year ends up getting the principal back. It becomes a long stream of predictable income passed down the line.

The second reason is trade. Bonds can be traded just like stocks. So a 100-year bond doesn’t mean you’re locked in for a century. You can buy it today and sell it later. If you believe that interest rates will fail (remember what we discussed earlier – when rates fall, bond prices rise), the value of your mortgage may increase, allowing you to sell it at a profit. For investors who expect rates to fall over time, this is a clear opportunity.

Another thing worth understanding is something called a mortgage’s duration. Simply put, it tells you how long it takes on average to recover what you paid for the mortgage through its interest payments and the final principal repayment. For Alphabet’s 100-year bond, the duration is net under 17 years. That’s much shorter than 100, and actually a pretty reasonable time horizon for many investors.

Duration also gives you a rough idea of how sensitive a tire is to interest rate changes. The higher the number, the more your mortgage’s price will move when interest rates change. As a rule of thumb, if a bond has a 10-year term, a 1% move in interest rates can change its price by about 10%. The same logic applies here. With a duration of around 17 years, even a small 0.25% rate cut can push the bond’s price up significantly, by around 4.25% (and vice versa). That said, remember that this is only an approximation. This works best for small changes in interest rates. For larger moves, the actual price change will not be perfectly linear.

So yes, if you read headlines that scream that investors are simply betting that Alphabet will still be around in 2126, that’s probably not the real reason they’re putting money into this.

And that’s more or less the mystery behind Alphabet’s rare 100-year bond.

Until next time…

If this story helped you understand 100-year bonds and why investors are willing to bet on them, share it with friends who googled it. Or even family and curious people who might enjoy learning something new via WhatsApp, LinkedInand x.

If you are an Indian living abroad, here is a question.

If something were to happen to you, would your family in India know how to deal with a foreign insurer? Different laws. Different time zones. And different claim processes.

Indian term insurance can make claims easier for families at home, and it’s often cheaper too.

But there are caveats: medical underwriting abroad, availability of riders, country restrictions, tax implications and documentation requirements.

So we have explained everything that NRIs need to know about buying term insurance in India.

Look at us detailed guide on term insurance for NRIs in India here.

![[keyword]](https://learnxyz.in/wp-content/uploads/2026/03/चीन-पर्याप्त-तेल-की-बात-कर-रहा-है-क्योंकि-ट्रम्प.jpeg)

![[keyword]](https://learnxyz.in/wp-content/uploads/2026/03/तेल-की-बढ़ती-कीमतों-के-बावजूद-फेड-को-अभी-भी.jpeg)