![[keyword]](https://learnxyz.in/wp-content/uploads/2026/02/1772014480_Global-MA-remains-strong-in-2026-despite-tightest-capital-squeeze.jpeg)

A Goldman Sachs logo is displayed on the floor of the New York Stock Exchange in New York City on Wednesday, August 11, 2010.

Ramin Talaie | Corbis Historical | Getty Images

The global mergers and acquisitions boom that defined 2025 is entering 2026 as companies rethink their portfolios and artificial intelligence-led demand fuels large-scale deals. However, an increasingly tight capital pool forces managers to be more selective than ever before.

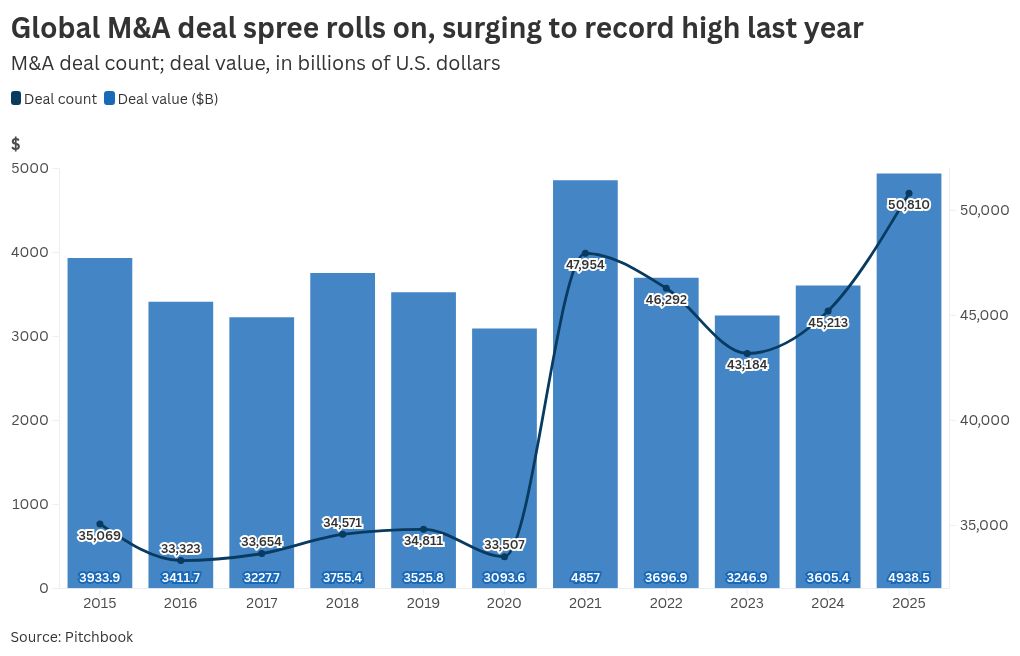

Despite a sluggish start, as Trump’s sweeping tariffs briefly stymied acquisitions and new public listings early last year, the total value of deal-making activity surged nearly 40% to a record $4.9 trillion in 2025, according to private market intelligence firm Pitchbook.

That surpassed the previous high of $4.86 trillion set in 2021 as deal count and value activity hit records, PitchBook said. Activity accelerated as central banks cut interest rates, valuations improved and companies increased spending on artificial intelligence.

Markets are betting the rally will continue as Wall Street regains its appetite for big deals amid the prospect of lower borrowing costs.

A Bain & Company survey of 300 M&A executives found that 80% expect to maintain or increase deal activity this year, citing improved macroeconomic conditions and a growing backlog of private equity and venture capital assets awaiting exit.

As abrupt shifts in trade policy settled into a pattern of less threatening change, relief turned to confidence and then a fear of missing out.

Jake Henry

Global co-leader, McKinsey’s M&A Practice.

Goldman Sachs, based on its own poll of 600 corporate and financial sponsor clients, found that 57% believe that scale and strategic growth will be the primary driver of deal decisions this year.

“As abrupt shifts in trade policies settled into a pattern of less threatening change, relief turned to confidence and then a fear of missing out,” said Jake Henry, global co-leader of McKinsey’s M&A Practice.

Central to the shift is a decisive push by companies to rethink their portfolios, as geopolitical risks, economic fragmentation and uneven global growth force boards to rethink where they operate and the risks they are willing to take.

“Leaders across industries recognize that many traditional business models have reached the limits of their historical growth engines,” said Suzanne Kumar, executive vice president of Bain’s global M&A and investment practice.

“Companies urgently need to reinvent themselves to get ahead of the major forces of technological disruption, a post-globalization economy and shifting profit pools,” Kumar added.

Goldman at the top of the global M&A rankings last year, advertising on nearly 40 deals worth $1.48 trillion in total volume. It was the strongest period for mega deals by volume, according to Reutersciting LSEG records dating back to 1980.

Still, companies remain cautious. Boston Consulting Group’s M&A sentiment index rebounded to 75 from its low at the end of 2022 — but still remained well below the long-term average of 100, “reflecting an improved but cautious attitude.” A higher value than the previous month indicates that M&A market momentum is accelerating, while a lower value suggests a slowdown.

The tightest funding in decades

While the appetite for deals remains strong, the pool of discretionary capital to fund them is historically thin, forcing managers to pursue only deals that deliver clear returns.

The proportion of capital allocated to M&A hit a 30-year low in 2025, according to Bain, as companies directed more cash to dividends, buybacks, capital expenditures as well as research and development.

“Executives need to pressure test whether M&A routes and specific deals will help the company better compete in the most attractive markets…rethink portfolio boundaries, and make bigger, bolder decisions about what capabilities to own versus access,” Kumar said.

“As competing demands for capital raise the bar for deals, disciplined reinvention and value creation are essential,” she added.

The financial crisis has driven private capital to the center of deals. Private equity firms are seeking to deploy idle cash, lenders are turning to private credit funds for flexibility, and sovereign wealth funds are increasingly acting as lead investors rather than passive backers.

Private equity now accounts for about 40% of global mergers and acquisition activity, according to Goldman. Despite signs of stress in the private credit market — now worth about $2.1 trillion — Goldman expects the asset class to more than double by 2030, broadening the pool of capital available to finance large deals.

AI capital spending ‘supercycle’

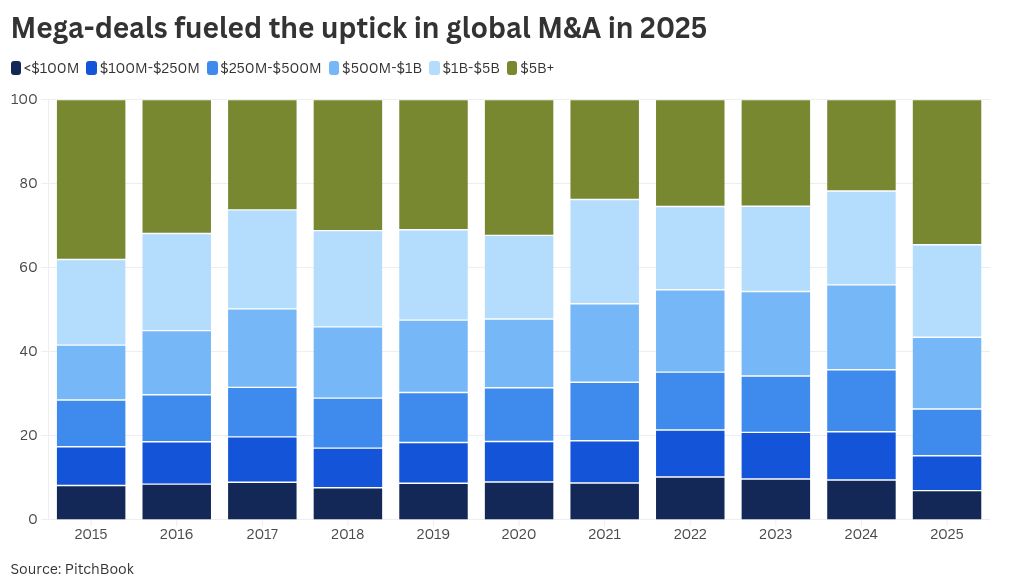

Blockbuster deals are fueling the resurgence in M&A, driven by AI-related demand, according to industry reports.

Mega deals worth more than $5 billion accounted for more than 73% of the increase in deal value in 2025, according to Bain.

The number of transactions that exceed the $10 billion threshold rose to 60 last year, the highest level since 2021, says McKinsey’s Henry.

“We expect more big deals in 2026, with continued consolidation and geographic expansion,” Henry said, with AI-related service providers fueling “big fever” this year.

However, the heavy capital spending on AI could limit M&A activity in the near term, said Brian Levy, global deal operations leader at PwC.

As AI adoption accelerates, the demand for computing power has risen across digital infrastructure, energy, semiconductors and hardware optimization. In response, many companies are choosing to acquire rather than build across the technology stack.

Between the first quarter of 2024 and the third quarter of last year, US hyperscalers’ capital spending averaged $760 million per day, according to Goldman Sachs.

The Wall Street bank estimates that another 65 gigawatts of data center capacity will be online by 2030 — more than double the amount added from 2019 to 2024.

“Investment in AI is directed at data centers, energy and other infrastructure, as well as technology development and adaptation,” Levy said.

“In the near term, the scale of this multitrillion-dollar investment could divert capital and dampen M&A activity.”

![[keyword]](https://learnxyz.in/wp-content/uploads/2026/04/चीन-विकास-मंच-बाजार-दबाव-में-सुधार-करने-वाले-अमेरिकी.jpeg)

![[keyword]](https://learnxyz.in/wp-content/uploads/2026/03/जीवन-चक्र-निधि-के-बारे-में-बताया-गया.jpg)

![[keyword]](https://learnxyz.in/wp-content/uploads/2026/04/अमेज़न-की-अगली-लड़ाई-ग्राहकों-के-लिए-नहीं-है.jpg)